A Hidden Markov Model (HMM) extends the mixture model by allowing the latent state to evolve over time according to a Markov chain. Where a mixture model treats each observation independently, an HMM captures temporal structure: the hidden state at time depends on the state at time .

This chapter covers:

The HMM generative model

Exact inference via the forward-backward algorithm

Learning parameters with EM (the Baum-Welch algorithm)

Source

import torch

import torch.distributions as dist

import matplotlib.pyplot as plt

import matplotlib.patches as mpatches

palette = list(plt.cm.Set2.colors)

torch.manual_seed(305)

<torch._C.Generator at 0x7f92601ec5d0>From Mixture Models to HMMs¶

Recall the Gaussian mixture model from Chapter 8:

The i.i.d. assumption means each data point is assigned to a cluster independently of its neighbours. For time-series data this is often unrealistic: a speaker stays in the same phoneme for multiple frames; a mouse stays in the same behavioural state for seconds.

The HMM replaces the i.i.d. prior on with a Markov chain:

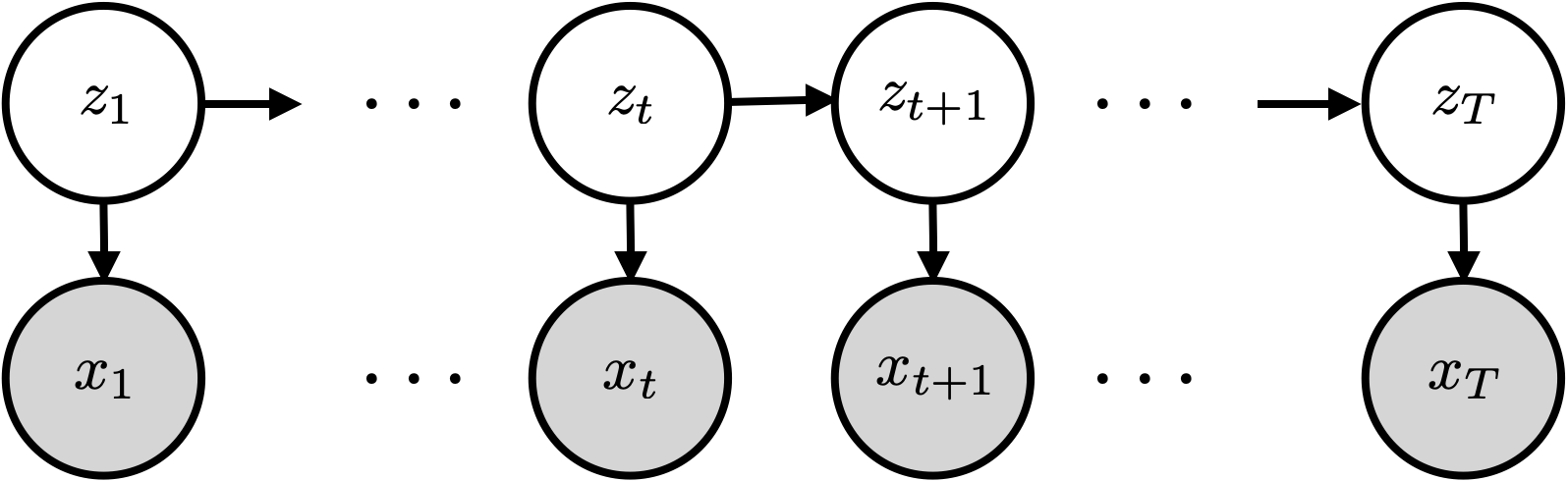

Graphical model for an HMM. The hidden states follow a Markov chain; each observation depends only on the current state .

The joint distribution factors as:

We call this an HMM because the hidden states follow a Markov chain, .

The Three Components¶

An HMM is defined by three ingredients:

Initial distribution — which state to start in.

Transition matrix (row-stochastic) — .

Emission distribution — Gaussian, categorical, Poisson, etc.

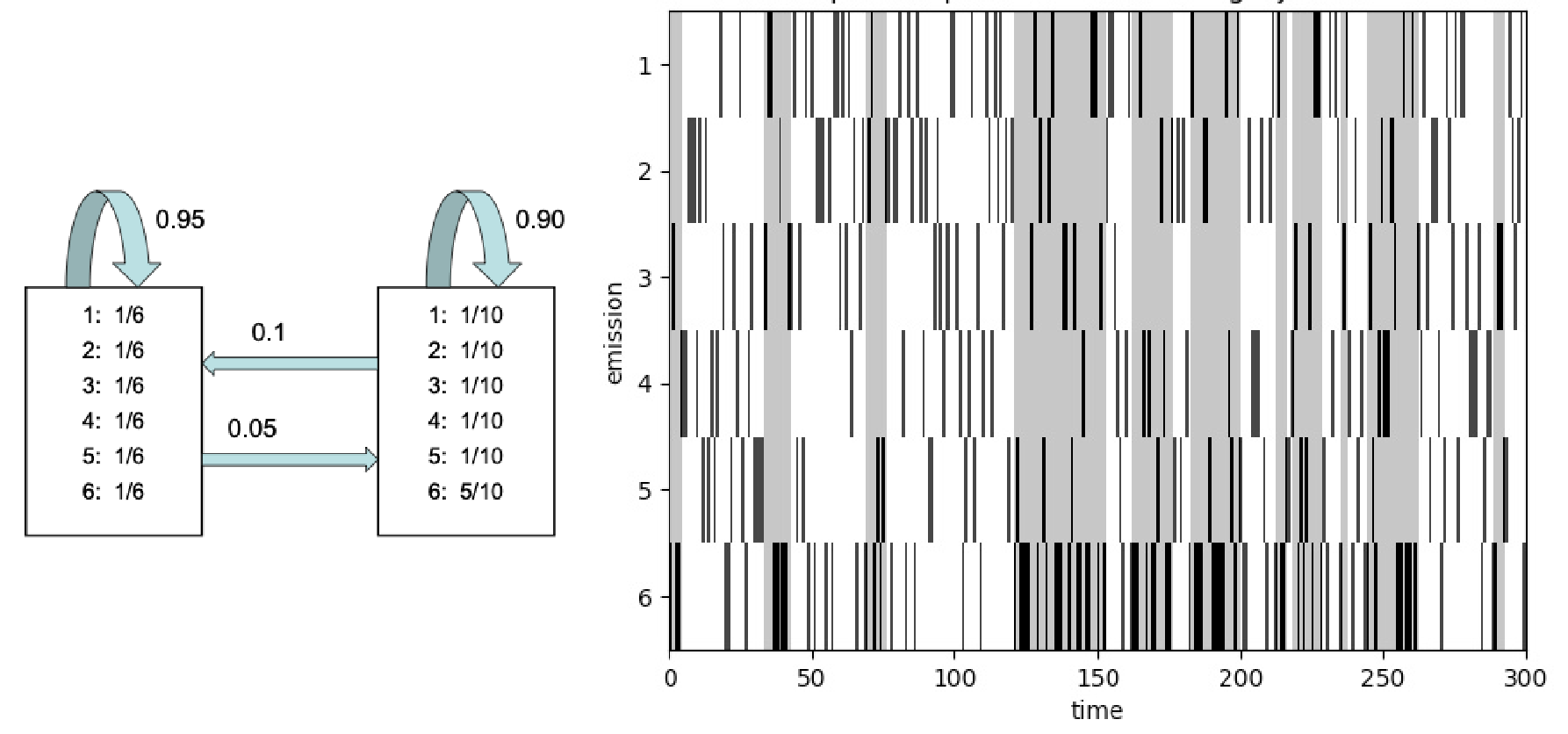

Example: The Dishonest Casino¶

An occasionally dishonest casino that switches between a fair die () and a loaded die (, ). Figure from dynamax.

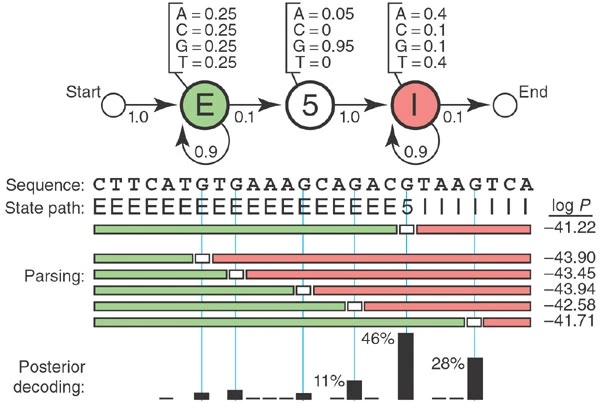

Example: Splice Site Recognition¶

A toy HMM for parsing a genome to find 5'' splice sites. Figure from Eddy, 2004.

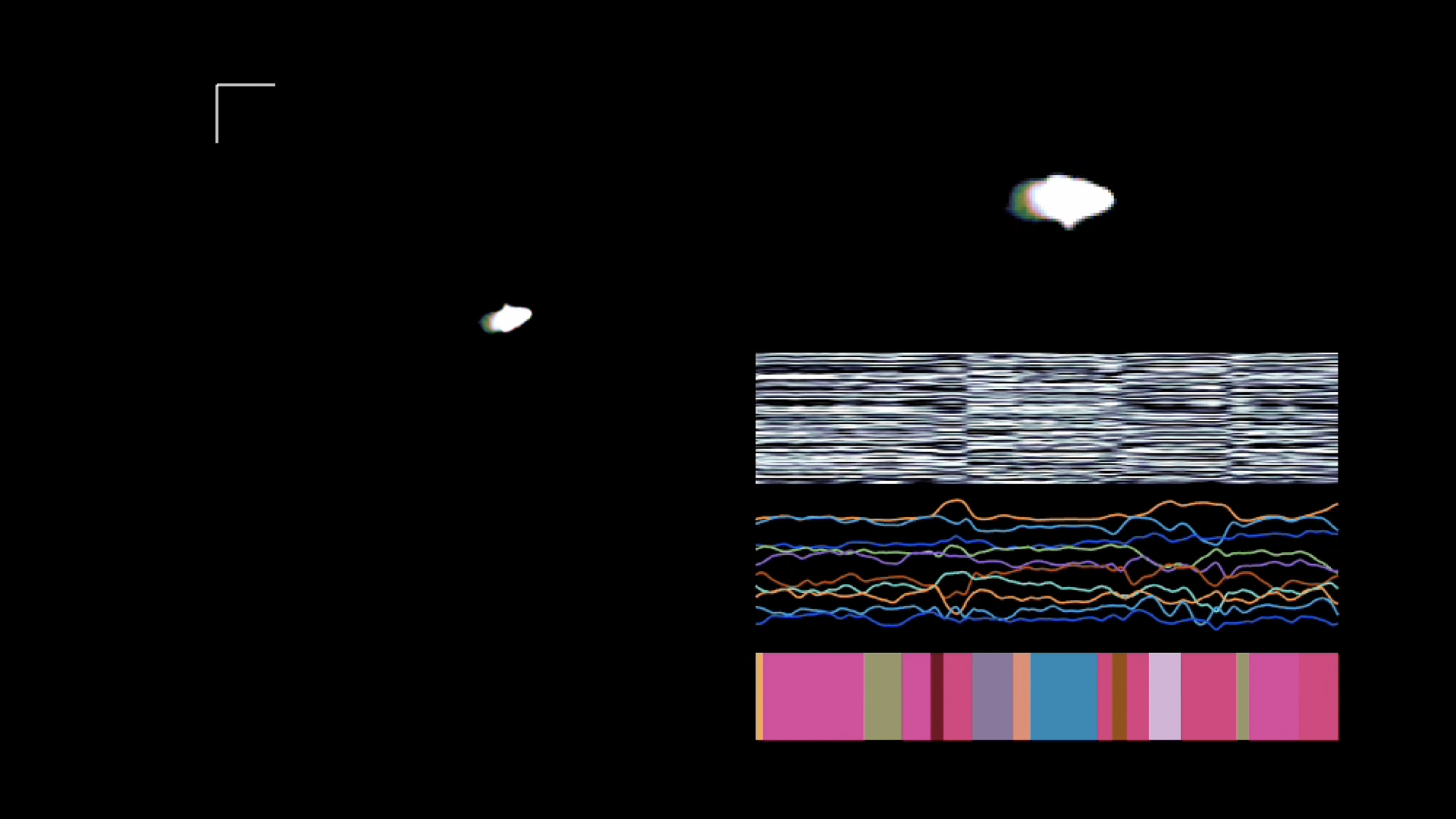

Example: Behavioural Segmentation of Video¶

Segmenting videos of freely moving mice with an autoregressive HMM. Figure from Wiltschko et al., 2015.

Inference Goals¶

Given observations and parameters , we want:

| Quantity | Name |

|---|---|

| Filtering — current state given past | |

| Smoothing — current state given all data | |

| Pairwise smoothing — needed for EM | |

| Viterbi — most likely path | |

| Marginal likelihood — needed for learning |

Why is naive enumeration expensive? Marginalising requires summing over state sequences. Message passing reduces this to by processing one time step at a time, exploiting the Markov structure.

The Forward Algorithm¶

Define the forward message at time as the joint probability of being in state and observing :

Base case: .

Recursion:

Let . In matrix form:

Normalizing for numerical stability. Re-normalize after each step:

The normalizers have a clean interpretation: is the predictive distribution , and . Therefore:

The Backward Algorithm and Smoothing¶

Define the backward message as the probability of future observations given the current state:

Base case: for all .

Recursion:

or in matrix form: .

Posterior Marginals (Smoothing)¶

Together the forward and backward passes give the forward-backward algorithm Rabiner & Juang, 1986.

Posterior Pairwise Marginals¶

These are needed for the EM M-step below.

EM for HMMs (Baum-Welch)¶

The ELBO for an HMM decomposes over the three parameter groups:

where (posterior marginals) and (posterior pairwise marginals).

E-step: Run the forward-backward algorithm to compute and .

M-step: The ELBO separates, giving closed-form updates:

For exponential family emissions, the weighted MLE for requires only the expected sufficient statistics — the same structure as the mixture model M-step.

# ── Forward-backward algorithm ────────────────────────────────────────────────

def forward_pass(log_pi0, log_P, log_likes):

'''Normalized forward messages.

Convention (matching the lecture):

log_alphas[t, k] = log p(z_t=k | x_{0:t-1}) (predictive, normalized)

log_norms[t] = log p(x_t | x_{0:t-1})

Args:

log_pi0: (K,) log initial distribution

log_P: (K, K) log_P[i,j] = log p(z_{t+1}=j | z_t=i)

log_likes: (T, K) log p(x_t | z_t=k)

Returns:

log_alphas (T, K), log_norms (T,)

'''

T, K = log_likes.shape

log_alphas = torch.zeros(T, K)

log_norms = torch.zeros(T)

log_alphas[0] = log_pi0 - torch.logsumexp(log_pi0, 0)

log_norms[0] = torch.logsumexp(log_alphas[0] + log_likes[0], 0)

for t in range(1, T):

log_joint = log_alphas[t-1] + log_likes[t-1] # (K,)

log_alpha_t = torch.logsumexp(log_joint[:, None] + log_P, 0) # (K,)

log_alphas[t] = log_alpha_t - torch.logsumexp(log_alpha_t, 0)

log_norms[t] = torch.logsumexp(log_alphas[t] + log_likes[t], 0)

return log_alphas, log_norms

def backward_pass(log_P, log_likes):

'''Normalized backward messages.

Args:

log_P: (K, K)

log_likes: (T, K)

Returns:

log_betas (T, K), with log_betas[T-1] = 0 (base case beta_T = 1)

'''

T, K = log_likes.shape

log_betas = torch.zeros(T, K) # base: beta_{T-1} = 1

for t in range(T - 2, -1, -1):

log_joint = log_likes[t+1] + log_betas[t+1] # (K,)

log_beta_t = torch.logsumexp(log_P + log_joint[None, :], 1) # (K,)

log_betas[t] = log_beta_t - torch.logsumexp(log_beta_t, 0)

return log_betas

def posterior_marginals(log_alphas, log_betas, log_likes):

'''gamma_t(k) = p(z_t=k | x_{0:T-1}). Returns (T, K).'''

log_gamma = log_alphas + log_likes + log_betas

log_gamma = log_gamma - torch.logsumexp(log_gamma, 1, keepdim=True)

return log_gamma.exp()

def posterior_pairs(log_alphas, log_betas, log_likes, log_P):

'''xi_t(i,j) = p(z_t=i, z_{t+1}=j | x_{0:T-1}). Returns (T-1, K, K).'''

T, K = log_alphas.shape

log_xi = (log_alphas[:-1, :, None]

+ log_likes[:-1, :, None]

+ log_P[None]

+ log_likes[1:, None, :]

+ log_betas[1:, None, :])

log_xi = log_xi - torch.logsumexp(log_xi.reshape(T-1, -1), 1).reshape(T-1, 1, 1)

return log_xi.exp()

# ── EM for an HMM with categorical emissions ──────────────────────────────────

def cat_log_likes(x, log_theta):

'''log p(x_t | z_t=k) for categorical emissions.

Args:

x: (T,) integer observations in {0, ..., V-1}

log_theta: (K, V) log emission probabilities

Returns:

(T, K)

'''

return log_theta[:, x].T

def em_hmm_cat(x, K, V, num_iters=60, seed=0):

'''Baum-Welch EM for a categorical-emission HMM.

Args:

x: (T,) integer observations in {0, ..., V-1}

K: number of hidden states

V: vocabulary size (number of emission symbols)

num_iters: EM iterations

Returns:

pi0 (K,), P (K, K), theta (K, V), ll_history

'''

torch.manual_seed(seed)

T = len(x)

# Random initialisation

pi0 = torch.ones(K) / K

P = torch.ones(K, K) / K

theta = torch.rand(K, V)

theta = theta / theta.sum(1, keepdim=True)

ll_history = []

for _ in range(num_iters):

# E-step

log_ll = cat_log_likes(x, theta.log())

log_alphas, log_norms = forward_pass(pi0.log(), P.log(), log_ll)

log_betas = backward_pass(P.log(), log_ll)

gamma = posterior_marginals(log_alphas, log_betas, log_ll) # (T, K)

xi = posterior_pairs(log_alphas, log_betas, log_ll, P.log()) # (T-1,K,K)

ll_history.append(log_norms.sum().item())

# M-step

pi0 = (gamma[0] + 1e-8) / (gamma[0] + 1e-8).sum()

xi_sum = xi.sum(0) + 1e-8 # (K, K)

P = xi_sum / xi_sum.sum(1, keepdim=True)

# Weighted counts for each emission symbol

x_oh = torch.zeros(T, V).scatter_(1, x.unsqueeze(1), 1.0) # (T, V) one-hot

counts = gamma.T @ x_oh + 1e-8 # (K, V)

theta = counts / counts.sum(1, keepdim=True)

return pi0, P, theta, ll_history

Source

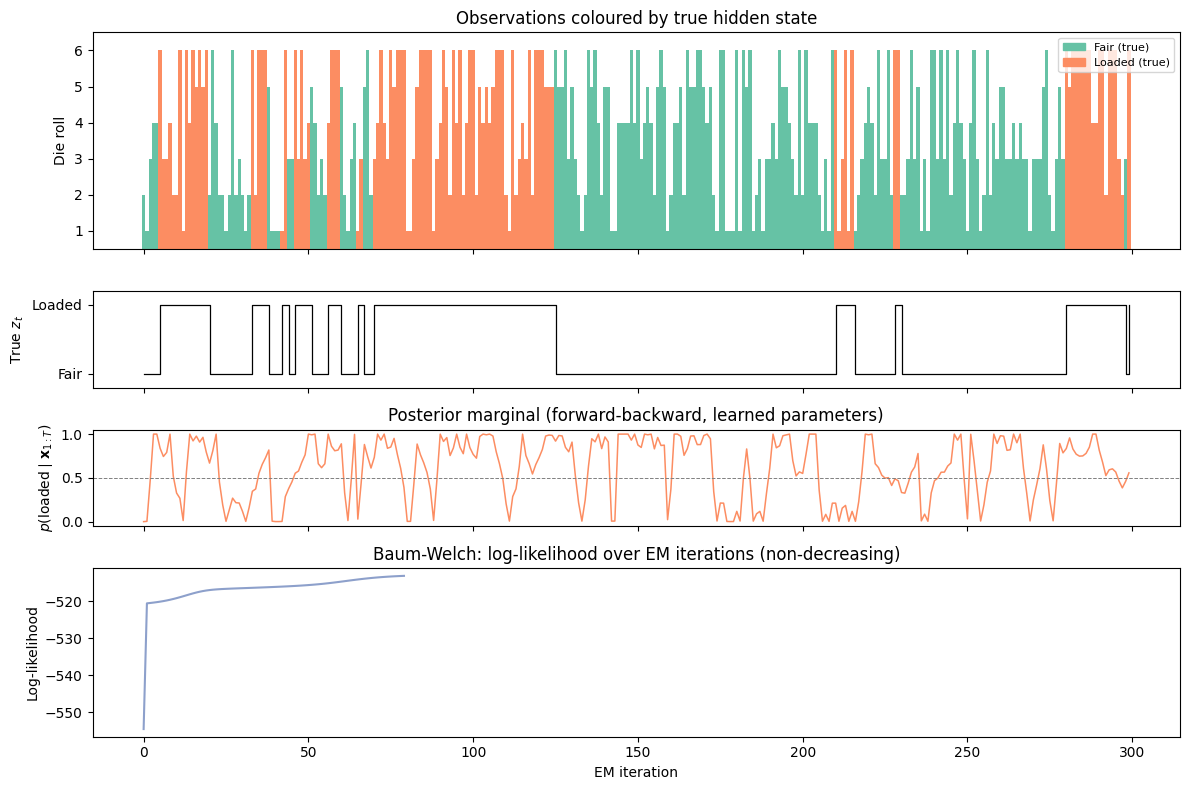

# ── Simulate from the dishonest casino ───────────────────────────────────────

K_true = 2 # states: 0=fair, 1=loaded

V = 6 # die faces 0..5

T_sim = 300

pi0_true = torch.tensor([1.0, 0.0])

P_true = torch.tensor([[0.95, 0.05],

[0.10, 0.90]])

theta_true = torch.tensor([[1/6]*6,

[0.1, 0.1, 0.1, 0.1, 0.1, 0.5]])

torch.manual_seed(42)

z_true = torch.zeros(T_sim, dtype=torch.long)

x_obs = torch.zeros(T_sim, dtype=torch.long)

z_true[0] = dist.Categorical(pi0_true).sample()

x_obs[0] = dist.Categorical(theta_true[z_true[0]]).sample()

for t in range(1, T_sim):

z_true[t] = dist.Categorical(P_true[z_true[t-1]]).sample()

x_obs[t] = dist.Categorical(theta_true[z_true[t]]).sample()

# ── Run EM to learn parameters ───────────────────────────────────────────────

pi0_em, P_em, theta_em, ll_hist = em_hmm_cat(x_obs, K=2, V=6, num_iters=80)

# Align states (EM may swap labels)

# State with higher p(6) should be "loaded"

loaded = theta_em[:, 5].argmax().item()

fair = 1 - loaded

# Posterior marginals with learned parameters

log_ll_em = cat_log_likes(x_obs, theta_em.log())

la, ln = forward_pass(pi0_em.log(), P_em.log(), log_ll_em)

lb = backward_pass(P_em.log(), log_ll_em)

gamma_em = posterior_marginals(la, lb, log_ll_em)

# ── Plot ──────────────────────────────────────────────────────────────────────

fig, axes = plt.subplots(4, 1, figsize=(12, 8), sharex=True,

gridspec_kw={'height_ratios': [1.8, 0.8, 0.8, 1.4]})

# Panel 1: die rolls coloured by true state

ax = axes[0]

colors = [palette[0] if z_true[t] == 0 else palette[1] for t in range(T_sim)]

ax.bar(range(T_sim), x_obs.numpy() + 1, color=colors, width=1.0, linewidth=0)

ax.set_ylabel('Die roll')

ax.set_ylim(0.5, 6.5)

ax.set_yticks([1, 2, 3, 4, 5, 6])

ax.set_title('Observations coloured by true hidden state')

fair_patch = mpatches.Patch(color=palette[0], label='Fair (true)')

loaded_patch = mpatches.Patch(color=palette[1], label='Loaded (true)')

ax.legend(handles=[fair_patch, loaded_patch], loc='upper right', fontsize=8)

# Panel 2: true hidden state sequence

ax = axes[1]

ax.step(range(T_sim), z_true.numpy(), where='post', color='k', lw=0.9)

ax.set_ylabel('True $z_t$')

ax.set_ylim(-0.2, 1.2)

ax.set_yticks([0, 1])

ax.set_yticklabels(['Fair', 'Loaded'])

# Panel 3: posterior p(loaded | all data) using learned parameters

ax = axes[2]

ax.plot(range(T_sim), gamma_em[:, loaded].numpy(), color=palette[1], lw=1.1)

ax.axhline(0.5, color='gray', linestyle='--', lw=0.7)

ax.set_ylabel('$p(\mathrm{loaded} \mid \mathbf{x}_{1:T})$')

ax.set_ylim(-0.05, 1.05)

ax.set_title('Posterior marginal (forward-backward, learned parameters)')

# Panel 4: ELBO / log-likelihood over EM iterations

ax = axes[3]

ax.plot(ll_hist, color=palette[2], lw=1.5)

ax.set_xlabel('EM iteration')

ax.set_ylabel('Log-likelihood')

ax.set_title('Baum-Welch: log-likelihood over EM iterations (non-decreasing)')

plt.tight_layout()

plt.show()

# Print learned vs true emission probabilities

print("Learned emission probs (fair die) :", theta_em[fair].numpy().round(3))

print("True emission probs (fair die) :", theta_true[0].numpy().round(3))

print()

print("Learned emission probs (loaded die):", theta_em[loaded].numpy().round(3))

print("True emission probs (loaded die):", theta_true[1].numpy().round(3))

print()

print(f"Learned transition matrix:\n{P_em.numpy().round(3)}")

print(f"True transition matrix:\n{P_true.numpy()}")

<>:63: SyntaxWarning: invalid escape sequence '\m'

<>:63: SyntaxWarning: invalid escape sequence '\m'

/tmp/ipykernel_2893/3219947313.py:63: SyntaxWarning: invalid escape sequence '\m'

ax.set_ylabel('$p(\mathrm{loaded} \mid \mathbf{x}_{1:T})$')

Learned emission probs (fair die) : [0.304 0.209 0.193 0. 0.02 0.274]

True emission probs (fair die) : [0.167 0.167 0.167 0.167 0.167 0.167]

Learned emission probs (loaded die): [0.002 0.101 0.149 0.236 0.201 0.311]

True emission probs (loaded die): [0.1 0.1 0.1 0.1 0.1 0.5]

Learned transition matrix:

[[0.703 0.297]

[0.188 0.812]]

True transition matrix:

[[0.95 0.05]

[0.1 0.9 ]]

Conclusion¶

| Component | Key idea |

|---|---|

| HMM | Mixture model with a Markov prior on |

| Forward pass | Recursive computation of |

| Backward pass | Recursive computation of |

| Forward-backward | Combines both to give |

| Baum-Welch / EM | E-step = forward-backward; M-step = weighted MLE |

Extensions worth knowing:

Viterbi algorithm: replaces with to find the most likely state sequence .

Autoregressive HMMs: each emission depends on both and recent observations Wiltschko et al., 2015.

Bayesian HMMs: place a Dirichlet prior on , rows of , and emission parameters; use Gibbs sampling or VI.

Infinite HMMs (iHMMs): nonparametric prior lets the number of states grow with the data.

- Wiltschko, A. B., Johnson, M. J., Iurilli, G., Peterson, R. E., Katon, J. M., Pashkovski, S. L., Abraira, V. E., Adams, R. P., & Datta, S. R. (2015). Mapping sub-second structure in mouse behavior. Neuron, 88(6), 1121–1135.

- Rabiner, L., & Juang, B. (1986). An introduction to hidden Markov models. Ieee Assp Magazine, 3(1), 4–16.