Poisson processes are fundamental stochastic models for random sets of points in time or space. In this chapter we study their defining properties, four ways to sample them, and how to go beyond simple Poisson models with self-exciting and doubly stochastic processes.

Source

import torch

import numpy as np

import matplotlib.pyplot as plt

from scipy.stats import beta as beta_dist, kstest

Defining Properties of a Poisson Process¶

A Poisson process is a stochastic process that generates a random set of points . It is governed by an intensity function .

Two key properties define a Poisson process:

Property 1 (Poisson counts): The number of points in any measurable set follows a Poisson distribution,

Property 2 (Independence): Counts on disjoint sets are independent,

![An inhomogeneous Poisson process on [0, T] with a time-varying intensity \lambda(t).](/stats305c/build/poisson_process-450ac16e751334a457c19ca425bee638.png)

An inhomogeneous Poisson process on with a time-varying intensity .

Common applications include modeling neural spike trains, locations of trees in a forest, arrival times of customers or web requests, and positions of photons on a detector.

Poisson Process Likelihood¶

From the top-down sampling procedure we can derive the likelihood. Given points :

This can be understood as: the probability that no point falls outside the observed set (the exponential factor) times the probability density at each observed location (the product term).

Four Ways to Sample a Poisson Process¶

1. Top-Down Sampling¶

For a Poisson process with intensity on domain :

Sample the total count .

Sample locations i.i.d. from the normalized intensity,

This requires the ability to compute the integral of and to sample from the normalized intensity.

2. Interval Sampling (Homogeneous Case)¶

A homogeneous Poisson process has constant intensity .

Property 3: Inter-arrival times are i.i.d. exponential,

Property 4 (Memoryless): The waiting time until the next point is independent of time elapsed since the last point.

Algorithm: start at , repeatedly sample and set , stopping when .

3. Time-Rescaling (Inhomogeneous Case)¶

Define the cumulative intensity . When everywhere, is invertible.

Algorithm:

Sample a homogeneous Poisson process with unit rate on to get .

Set .

This is the point-process analog of inverse-CDF sampling.

4. Thinning (Rejection Sampling)¶

Given a bounded intensity :

Sample a homogeneous Poisson process with rate to get candidate points.

Independently accept each candidate with probability .

This is the point-process analog of rejection sampling.

def sample_pp_topdown(intensity_fn, total_intensity, sample_location_fn, T):

'''Sample an inhomogeneous Poisson process using the top-down method.

Args:

intensity_fn: callable, intensity at a point

total_intensity: integral of intensity over [0, T]

sample_location_fn: callable returning one sample from normalized intensity

T: end of interval

Returns:

sorted array of event times

'''

N = torch.poisson(torch.tensor(total_intensity)).int().item()

events = torch.tensor([sample_location_fn() for _ in range(N)])

return events.sort().values

def sample_pp_intervals(lam, T):

'''Sample a homogeneous Poisson process on [0, T] via inter-arrival intervals.

Args:

lam: rate (scalar)

T: end of interval

Returns:

1D tensor of event times

'''

events = []

t = 0.0

while True:

dt = torch.distributions.Exponential(torch.tensor(lam)).sample().item()

t += dt

if t > T:

break

events.append(t)

return torch.tensor(events)

def sample_pp_thinning(intensity_fn, lam_max, T, dt=1e-3):

'''Sample an inhomogeneous Poisson process on [0, T] via thinning.

Args:

intensity_fn: callable mapping time -> intensity (must be <= lam_max)

lam_max: upper bound on intensity

T: end of interval

dt: time resolution (unused here; thinning uses continuous time)

Returns:

1D tensor of accepted event times

'''

candidates = sample_pp_intervals(lam_max, T)

accepted = []

for t in candidates:

prob = intensity_fn(t.item()) / lam_max

if torch.rand(1).item() < prob:

accepted.append(t.item())

return torch.tensor(accepted)

Source

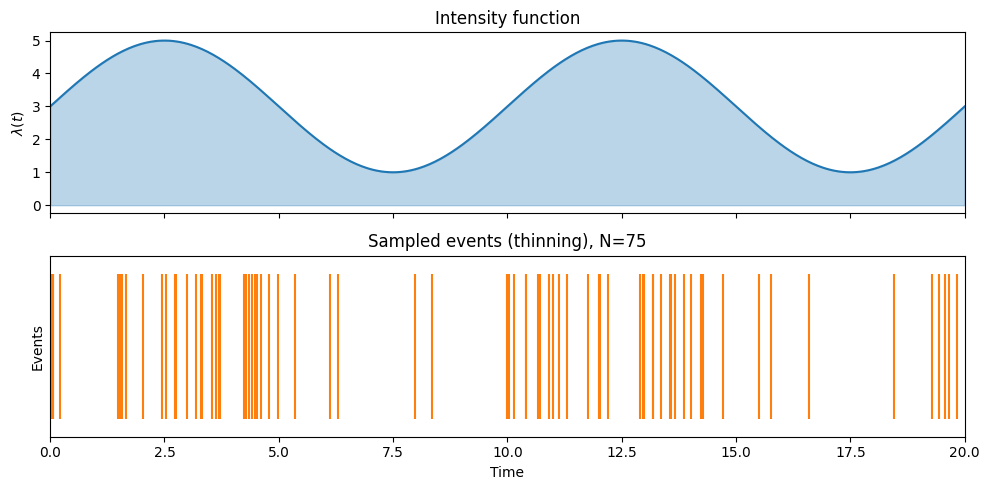

torch.manual_seed(42)

np.random.seed(42)

T = 20.0

# Define a sinusoidal intensity: lambda(t) = 3 + 2*sin(pi*t/5)

def intensity(t):

return 3.0 + 2.0 * np.sin(np.pi * t / 5.0)

lam_max = 5.0

total_lam = 3.0 * T # integral of constant part; sin integrates to 0

fig, axes = plt.subplots(2, 1, figsize=(10, 5), sharex=True)

# Plot intensity

ts = np.linspace(0, T, 500)

axes[0].fill_between(ts, intensity(ts), alpha=0.3, color='tab:blue')

axes[0].plot(ts, intensity(ts), color='tab:blue')

axes[0].set_ylabel(r'$\lambda(t)$')

axes[0].set_title('Intensity function')

# Sample via thinning

events_thin = sample_pp_thinning(intensity, lam_max, T)

axes[1].eventplot(events_thin.numpy(), lineoffsets=0.5, linelengths=0.8, color='tab:orange')

axes[1].set_ylabel('Events')

axes[1].set_xlabel('Time')

axes[1].set_title(f'Sampled events (thinning), N={len(events_thin)}')

axes[1].set_xlim(0, T)

axes[1].set_ylim(0, 1)

axes[1].set_yticks([])

plt.tight_layout()

plt.savefig('poisson_demo.png', dpi=100, bbox_inches='tight')

plt.show()

Superposition and Thinning¶

Property 5 (Superposition): The union of independent Poisson processes is also a Poisson process. If

then their union .

Poisson thinning is the reverse: given , independently assign each point to process 1 with probability . The resulting subsets are independent Poisson processes with intensities and respectively.

Goodness-of-Fit Test via Time-Rescaling¶

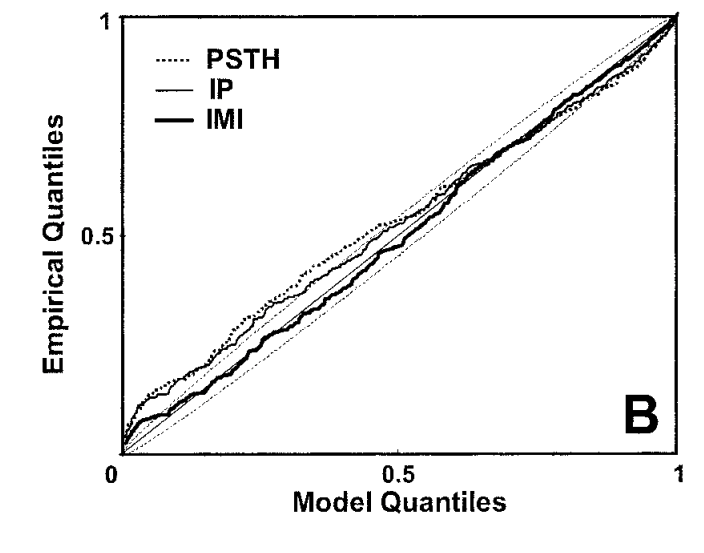

Brown et al., 2002 developed a powerful goodness-of-fit test for inhomogeneous Poisson processes based on the time-rescaling theorem.

Procedure: Given observed points and a fitted intensity :

Compute the rescaled inter-arrival intervals with . Under the correct model, .

Transform to uniform samples: . Under the correct model, .

Sort to get order statistics .

Plot — under the correct model this should fall near the 45° line.

Confidence bands: The -th order statistic follows . Use the 2.5% and 97.5% quantiles to build confidence bands.

Figure 1 from Brown et al., 2002: the time-rescaling Q–Q plot for a neural spike train model. Points within the confidence bands indicate a good fit.

Source

np.random.seed(0)

# True process: inhomogeneous PP with lambda(t) = 2 + sin(pi*t/5)

T_gof = 50.0

def true_intensity(t):

return 2.0 + np.sin(np.pi * t / 5.0)

def cum_intensity(t):

# Lambda(t) = 2t - (5/pi)*cos(pi*t/5) + 5/pi

return 2.0 * t - (5.0 / np.pi) * np.cos(np.pi * t / 5.0) + 5.0 / np.pi

# Sample events via thinning

lam_max_gof = 3.1

events_np = sample_pp_thinning(true_intensity, lam_max_gof, T_gof).numpy()

N_obs = len(events_np)

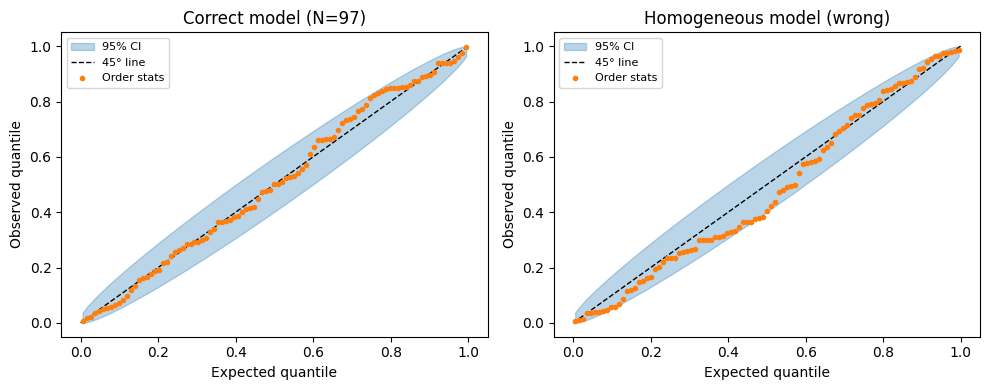

def gof_plot(ax, events, intensity_fn, cum_intensity_fn, T, title):

'''KS / time-rescaling goodness-of-fit Q-Q plot.'''

xs = np.sort(events)

# compute Lambda differences

xs_with_zero = np.concatenate([[0.0], xs])

Lambda_vals = np.array([cum_intensity_fn(t) for t in xs_with_zero])

Delta = np.diff(Lambda_vals)

z = 1 - np.exp(-Delta)

z_sorted = np.sort(z)

n_pts = len(z_sorted)

ns = np.arange(1, n_pts + 1)

expected = (ns - 0.5) / n_pts

# Beta confidence bands

lower = beta_dist.ppf(0.025, ns, n_pts - ns + 1)

upper = beta_dist.ppf(0.975, ns, n_pts - ns + 1)

ax.fill_between(expected, lower, upper, alpha=0.3, color='tab:blue', label='95% CI')

ax.plot([0, 1], [0, 1], 'k--', lw=1, label='45° line')

ax.plot(expected, z_sorted, 'o', ms=3, color='tab:orange', label='Order stats')

ax.set_xlabel('Expected quantile')

ax.set_ylabel('Observed quantile')

ax.set_title(title)

ax.legend(fontsize=8)

fig, axes = plt.subplots(1, 2, figsize=(10, 4))

# Good fit: use the true intensity

gof_plot(axes[0], events_np, true_intensity, cum_intensity,

T_gof, f'Correct model (N={N_obs})')

# Poor fit: use a constant (wrong) rate

lam_wrong = N_obs / T_gof

def cum_wrong(t):

return lam_wrong * t

gof_plot(axes[1], events_np, lambda t: lam_wrong, cum_wrong,

T_gof, f'Homogeneous model (wrong)')

plt.tight_layout()

plt.savefig('gof_demo.png', dpi=100, bbox_inches='tight')

plt.show()

Hawkes Processes¶

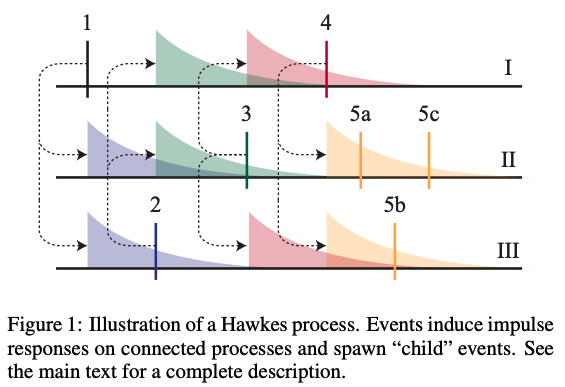

Hawkes processes Hawkes, 1971 are self-exciting point processes whose conditional intensity depends on the history of past events.

The conditional intensity is,

where is a non-negative impulse response (or influence function) and is the history up to time .

A common choice is an exponential impulse response,

where is the time constant and is the total weight (i.e., the expected number of events triggered per event, ).

Maximum Likelihood Estimation¶

The Hawkes log-likelihood has the same form as the Poisson process likelihood,

With an exponential impulse response and parameters , this simplifies to,

where and .

Multivariate Hawkes Processes¶

A multivariate Hawkes process Linderman & Adams, 2014 models interacting sources with mutually excitatory interactions,

where is a directed impulse response from source to source .

The weights with define a directed network of interactions.

Example from Linderman & Adams, 2014: inferred network structure from a multivariate Hawkes process fit to neural spike train data.

Hawkes Processes as Poisson Clustering¶

By the superposition principle, the points from each source can be decomposed into clusters:

where are background events and are events triggered by the -th event. With exponential impulse responses, .

This clustering representation enables a Gibbs sampler for Bayesian inference: with a Gamma prior , the weights and cluster assignments have conjugate conditionals that can be sampled alternately.

Source

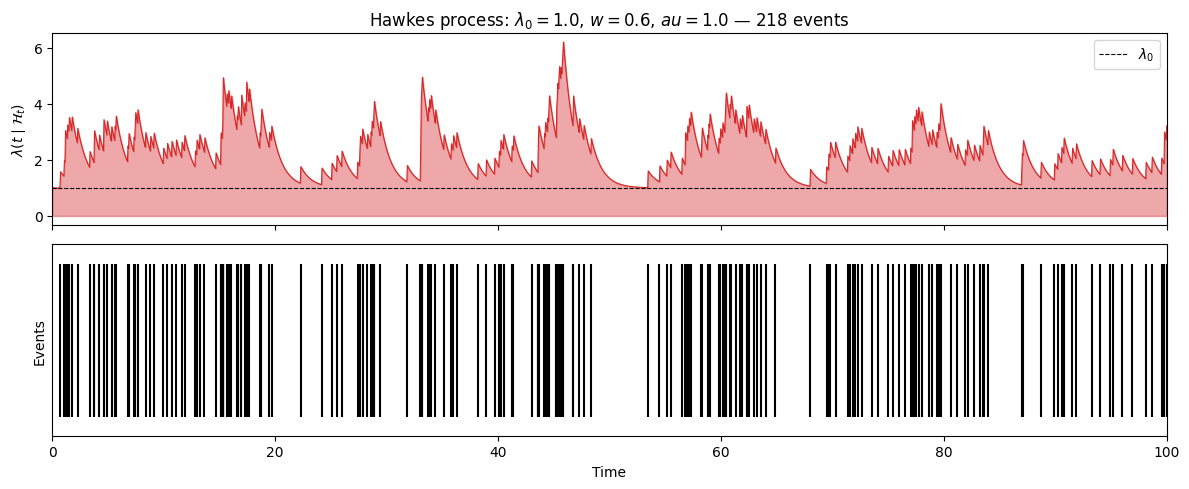

def sample_hawkes(lam0, w, tau, T, seed=0):

'''Sample a univariate Hawkes process with exponential impulse response.

Args:

lam0: baseline intensity

w: excitation weight (expected offspring per event)

tau: time constant of exponential impulse response

T: end of interval

seed: random seed

Returns:

sorted numpy array of event times

'''

rng = np.random.default_rng(seed)

events = []

t = 0.0

# Use Ogata's thinning algorithm

while t < T:

# Upper bound on intensity given current history

lam_bar = lam0 + (w / tau) * sum(np.exp(-(t - ti) / tau) for ti in events)

# Next candidate event

dt = rng.exponential(1.0 / lam_bar)

t_cand = t + dt

if t_cand > T:

break

# Evaluate true intensity at candidate

lam_cand = lam0 + (w / tau) * sum(np.exp(-(t_cand - ti) / tau) for ti in events)

# Accept/reject

if rng.uniform() < lam_cand / lam_bar:

events.append(t_cand)

t = t_cand

return np.array(sorted(events))

T_hawkes = 100.0

events_hawkes = sample_hawkes(lam0=1.0, w=0.6, tau=1.0, T=T_hawkes, seed=7)

N_hawkes = len(events_hawkes)

# Plot: event raster + conditional intensity

ts_h = np.linspace(0, T_hawkes, 2000)

tau_h = 1.0

lam0_h = 1.0

w_h = 0.6

lam_t = np.array([

lam0_h + (w_h / tau_h) * sum(np.exp(-(t - ti) / tau_h) for ti in events_hawkes if ti < t)

for t in ts_h

])

fig, axes = plt.subplots(2, 1, figsize=(12, 5), sharex=True)

axes[0].fill_between(ts_h, lam_t, alpha=0.4, color='tab:red')

axes[0].plot(ts_h, lam_t, color='tab:red', lw=0.8)

axes[0].axhline(lam0_h, ls='--', color='k', lw=0.8, label=r'$\lambda_0$')

axes[0].set_ylabel(r'$\lambda(t \mid \mathcal{H}_t)$')

axes[0].set_title(f'Hawkes process: $\lambda_0={lam0_h}$, $w={w_h}$, $\tau={tau_h}$ — {N_hawkes} events')

axes[0].legend()

axes[1].eventplot(events_hawkes, lineoffsets=0.5, linelengths=0.8, color='k')

axes[1].set_xlabel('Time')

axes[1].set_ylabel('Events')

axes[1].set_yticks([])

axes[1].set_xlim(0, T_hawkes)

axes[1].set_ylim(0, 1)

plt.tight_layout()

plt.savefig('hawkes_demo.png', dpi=100, bbox_inches='tight')

plt.show()

print(f"Average rate: {N_hawkes / T_hawkes:.2f} (expected: {lam0_h / (1 - w_h):.2f})")

<>:53: SyntaxWarning: invalid escape sequence '\l'

<>:53: SyntaxWarning: invalid escape sequence '\l'

/tmp/ipykernel_3022/3277385441.py:53: SyntaxWarning: invalid escape sequence '\l'

axes[0].set_title(f'Hawkes process: $\lambda_0={lam0_h}$, $w={w_h}$, $\tau={tau_h}$ — {N_hawkes} events')

Average rate: 2.18 (expected: 2.50)

Doubly Stochastic (Cox) Processes¶

Hawkes processes introduce dependence through the past. An alternative is to model the intensity itself as a random process — these are called doubly stochastic processes or Cox processes.

In these models,

and then, given , the points are generated as a Poisson process with that intensity.

Log Gaussian Cox process: Let and set . This gives a flexible, non-negative intensity with a log-Gaussian marginal distribution at each point.

Sigmoidal Gaussian Cox process Adams et al., 2009: Use where is the sigmoid function. This allows exact inference via a thinning construction.

Neyman–Scott process Wang et al., 2022: Let be a convolution of a Poisson process with a non-negative kernel. This generates clustered point patterns where events arise in groups.

The key challenge in all these models is computing (or approximating) the intractable integral in the likelihood.

Summary¶

Poisson processes are defined by an intensity function and two properties: Poisson counts and independence of disjoint sets.

They can be sampled by four methods: top-down, intervals (homogeneous), time-rescaling, and thinning (rejection sampling).

The time-rescaling theorem yields a simple goodness-of-fit test: if the model is correct, the rescaled intervals are i.i.d. , and after a further transformation, the order statistics fall along a 45° line.

Hawkes processes introduce self-excitation via a conditional intensity that depends on past events; their clustering representation enables efficient Bayesian inference.

Cox processes introduce dependence by modeling the intensity as a stochastic process, typically a Gaussian process transformed to be non-negative.

- Brown, E. N., Barbieri, R., Ventura, V., Kass, R. E., & Frank, L. M. (2002). The time-rescaling theorem and its application to neural spike train data analysis. Neural Computation, 14(2), 325–346.

- Hawkes, A. G. (1971). Spectra of some self-exciting and mutually exciting point processes. Biometrika, 58(1), 83–90.

- Linderman, S., & Adams, R. (2014). Discovering latent network structure in point process data. International Conference on Machine Learning, 1413–1421.

- Adams, R. P., Murray, I., & MacKay, D. J. (2009). Tractable nonparametric Bayesian inference in Poisson processes with Gaussian process intensities. Proceedings of the 26th Annual International Conference on Machine Learning, 9–16.

- Wang, Y., Degleris, A., Williams, A. H., & Linderman, S. W. (2022). Spatiotemporal Clustering with Neyman-Scott Processes via Connections to Bayesian Nonparametric Mixture Models. arXiv Preprint arXiv:2201.05044.